Blab Entertainment

Institutional Investors Ramp Up Netflix Holdings in Q1 2026, Reflecting Strong Subscriber Growth and Advertising Momentum

When the Q1 2026 13F filings were released, a chorus of institutional investors announced fresh stakes in Netflix, signaling renewed confidence in the streaming giant’s long‑term prospects.

The largest additions came from Jeremy Grantham’s Grantham, Mayo, Van Otterloo & Co. LLC (GMO), Tom Russo of Gardner Russo & Quinn LLC, Cliff Asness of AQR Capital Management, and Joel Greenblatt’s Gotham Asset Management. GMO added 4,049,031 shares—an increase of 4,016,502 shares—valued at roughly $390 million. Russo raised his holding by 605,901 shares, worth about $540 million. AQR’s stake grew by 283,941 shares, translating to approximately $280 million, while Gotham bought an additional 160,043 shares, worth $50 million. Smaller yet noteworthy moves included Bridgewater Associates, which added 59,584 shares ($10 million), and GAMCO Investors, which added 20,505 shares ($10 million). Steve Cohen’s Point 72 Asset Management entered a new position of 230,000 shares ($20 million), and Chris Bloomstran’s Semper Augustus Investments Group added 2,980 shares—a modest $0.00 million.

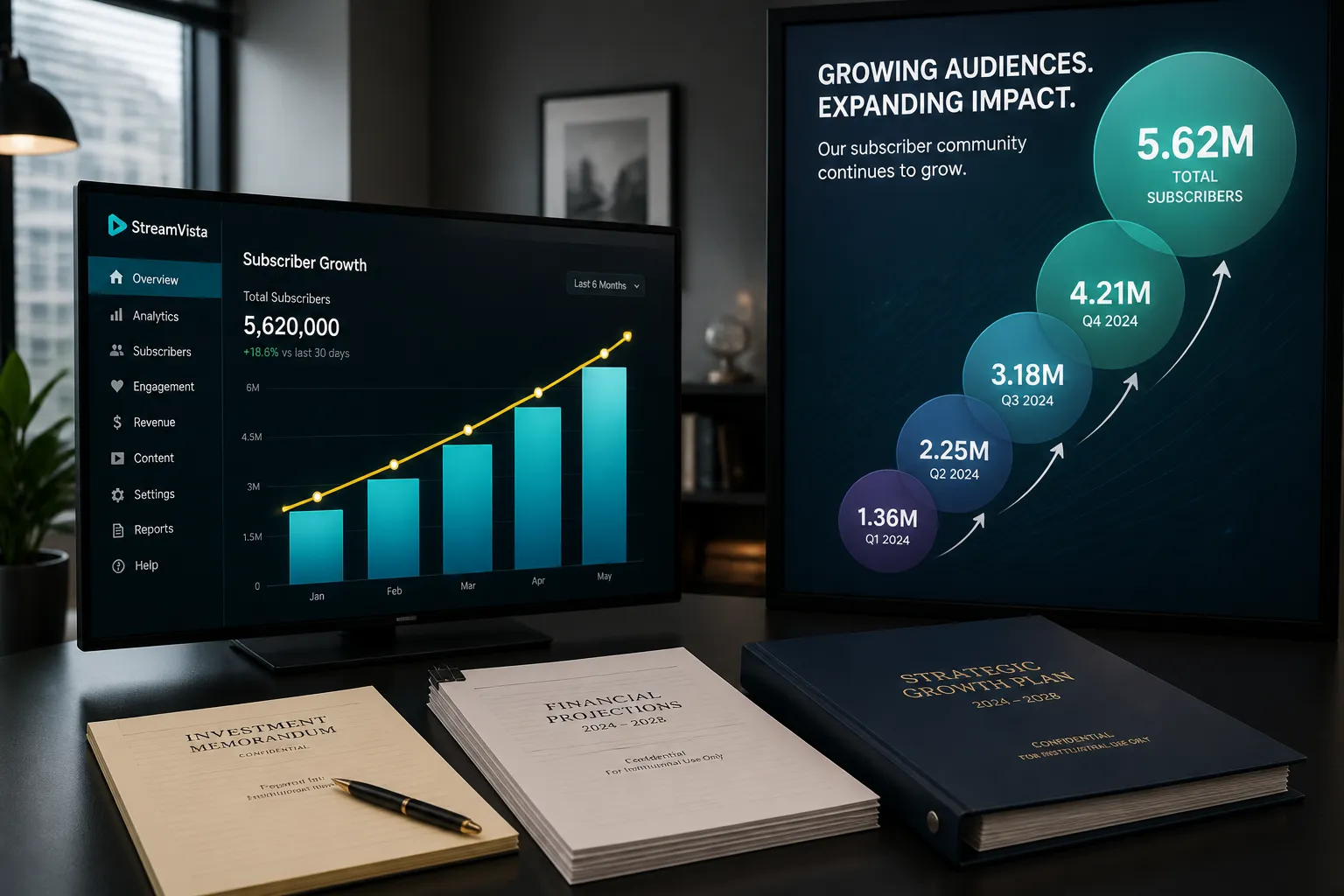

These purchases arrive on the heels of Netflix’s announcement of a 325 million‑user paid subscriber base spread across more than 190 countries. Q1 2026 revenue topped $12.25 billion, a 16% year‑over‑year rise that underscores the company’s continued growth.

The advertising arm is also accelerating. Ad revenue is on track to double, and more than 4,000 advertisers now run campaigns on the platform. Operating margin sits at 28.15% on a trailing‑12‑month basis, with management targeting 31.5% for 2026. Free cash flow remains robust, providing the liquidity needed to fund content and technology investments.

The concentration of buying among quantitative, value‑oriented, and long‑term investors suggests that Netflix’s dominant market position and its ability to monetize a large global audience through both subscription and advertising streams are viewed as solid fundamentals. Analysts point to the firm’s continued subscriber growth, coupled with a maturing advertising model, as a diversified revenue base capable of sustaining margin expansion.

From an industry perspective, Netflix’s performance reaffirms the relevance of a hybrid model that blends paid subscriptions with a growing ad‑supported tier. The company’s ability to attract institutional capital amid increasing competition from other streaming services indicates that investors see Netflix as a resilient franchise with durable competitive advantages.

Today, Netflix’s shareholder base is expanding, its subscriber and advertising metrics are improving, and its operating profile is strengthening. The company will continue to report quarterly results and update guidance on margin targets and free cash flow. Institutional investors will likely keep a close eye on Netflix’s advertising expansion and content investment plans as the next key drivers of growth.

The largest additions came from Jeremy Grantham’s Grantham, Mayo, Van Otterloo & Co. LLC (GMO), Tom Russo of Gardner Russo & Quinn LLC, Cliff Asness of AQR Capital Management, and Joel Greenblatt’s Gotham Asset Management. GMO added 4,049,031 shares—an increase of 4,016,502 shares—valued at roughly $390 million. Russo raised his holding by 605,901 shares, worth about $540 million. AQR’s stake grew by 283,941 shares, translating to approximately $280 million, while Gotham bought an additional 160,043 shares, worth $50 million. Smaller yet noteworthy moves included Bridgewater Associates, which added 59,584 shares ($10 million), and GAMCO Investors, which added 20,505 shares ($10 million). Steve Cohen’s Point 72 Asset Management entered a new position of 230,000 shares ($20 million), and Chris Bloomstran’s Semper Augustus Investments Group added 2,980 shares—a modest $0.00 million.

These purchases arrive on the heels of Netflix’s announcement of a 325 million‑user paid subscriber base spread across more than 190 countries. Q1 2026 revenue topped $12.25 billion, a 16% year‑over‑year rise that underscores the company’s continued growth.

The advertising arm is also accelerating. Ad revenue is on track to double, and more than 4,000 advertisers now run campaigns on the platform. Operating margin sits at 28.15% on a trailing‑12‑month basis, with management targeting 31.5% for 2026. Free cash flow remains robust, providing the liquidity needed to fund content and technology investments.

The concentration of buying among quantitative, value‑oriented, and long‑term investors suggests that Netflix’s dominant market position and its ability to monetize a large global audience through both subscription and advertising streams are viewed as solid fundamentals. Analysts point to the firm’s continued subscriber growth, coupled with a maturing advertising model, as a diversified revenue base capable of sustaining margin expansion.

From an industry perspective, Netflix’s performance reaffirms the relevance of a hybrid model that blends paid subscriptions with a growing ad‑supported tier. The company’s ability to attract institutional capital amid increasing competition from other streaming services indicates that investors see Netflix as a resilient franchise with durable competitive advantages.

Today, Netflix’s shareholder base is expanding, its subscriber and advertising metrics are improving, and its operating profile is strengthening. The company will continue to report quarterly results and update guidance on margin targets and free cash flow. Institutional investors will likely keep a close eye on Netflix’s advertising expansion and content investment plans as the next key drivers of growth.